Bank resolution

Information on bank resolution and creditor participation (bail-in)

In response to the 2008 financial crisis, several countries have enacted regulations that enable banks at risk of collapse to be systematically resolved in the future without requiring taxpayers’ participation. As a result, shareholders and creditors of a bank at risk may be required to participate in bearing the bank’s losses. The objective is to make it possible to resolve a bank without using public funds.

To this effect, the European Union has adopted the following legislation:

- the Bank Recovery and Resolution Directive (BRRD)

- and the regulation to establish uniform rules and a uniform procedure for the resolution of credit institutions and certain investment firms under a single resolution mechanism and a single resolution fund (SRM Regulation).

The BRRD requires, among other things, that each member state of the EU establishes a national resolution authority that has certain rights for the resolution and recovery of credit institutions. These measures may adversely affect bank shareholders and creditors.

The exact details of the measures that can be taken by resolution authorities may differ at a national level. In the following, we will use Germany as a model to explain the possible resolution measures. Other countries’ resolution processes, particularly those of non-European countries, may also differ and have even stronger implications.

Who could be affected?

If you are a shareholder or creditor of a bank, you may be affected if you hold financial instruments issued by the bank (e.g. shares, bonds, or certificates), or if you are a contractual partner of the bank and have claims against the bank (e.g. individual transactions under a master agreement for financial futures).

Securities that you, as a custodial customer of the bank, have held in a securities account and that are not issued by the bank, are not subject to a resolution measure against that bank. In the event that a custodian bank is resolved, your ownership rights to the financial instruments in the securities account will remain unaffected.

Who are the resolution authorities?

Resolution authorities have been appointed to facilitate a structured resolution in the event of a crisis. The resolution authority responsible for the bank concerned is authorized to order resolution measures under certain resolution conditions.

The Single Resolution Board (SRB) and the Federal Agency for Financial Market Stabilization (FMSA) are the resolution authorities responsible in Germany. For the sake of simplicity, no further distinction is made between the SRB and the FMSA below.

When would bank resolution or creditor participation take place?

The resolution authority may order certain resolution measures if the following resolution requirements are met:

- The bank in question is at risk of failing to survive in its present form. This assessment is made in accordance with statutory requirements and exists, for example, if the bank no longer meets the statutory requirements for licensing as a credit institution due to losses.

- There is no chance of preventing the bank’s failure through alternative measures taken by the private sector or other measures taken by the supervisory authorities.

- The measure is required for public interest, i.e. necessary and proportionate, and a regular liquidation process to resolve the bank is not an equivalent alternative.

What measures can the resolution authority take?

If all resolution requirements are met, the resolution authority can take extensive resolution measures – even before insolvency – which may have a negative impact on the bank’s shareholders and creditors:

- The bail-in tool (also known as creditor participation): The resolution authority can either partially or fully write down financial instruments of and claims against the bank, or convert them into equity (shares or other company interests) as a means of stabilizing the bank.

- The sale of business tool: In this process, shares, assets, rights, or liabilities of the bank under resolution are fully or partially sold to a specific buyer. If the shareholders and creditors are affected by the sale of the business, they will face another existing institution.

- The bridge institution tool: The resolution authority may transfer shares in the bank – a portion or all of the bank’s assets, including its liabilities – to what is known as a bridge institution. This may affect the bank’s ability to meet its payment and delivery obligations to creditors, as well as reduce the value of the shares in the bank.

- The transfer to an asset management company: Assets, rights, or liabilities are transferred to a separate asset management entity. The aim of this is to manage the assets to maximize their value until their subsequent sale or liquidation. As in the case of business sales, a creditor is faced with a new debtor once the transfer has taken place.

The resolution authority may, through an official order, adjust the terms and conditions of the financial instruments issued by the bank as well as the claims existing against it, including, for example, changing the due date or the interest rate to the detriment of the creditor. Furthermore, payment and delivery obligations may be modified, including being temporarily suspended. Termination and other rights of creditors under the financial instruments or receivables may also be temporarily suspended.

Under what circumstances might I, as a creditor, be affected by a bail-in?

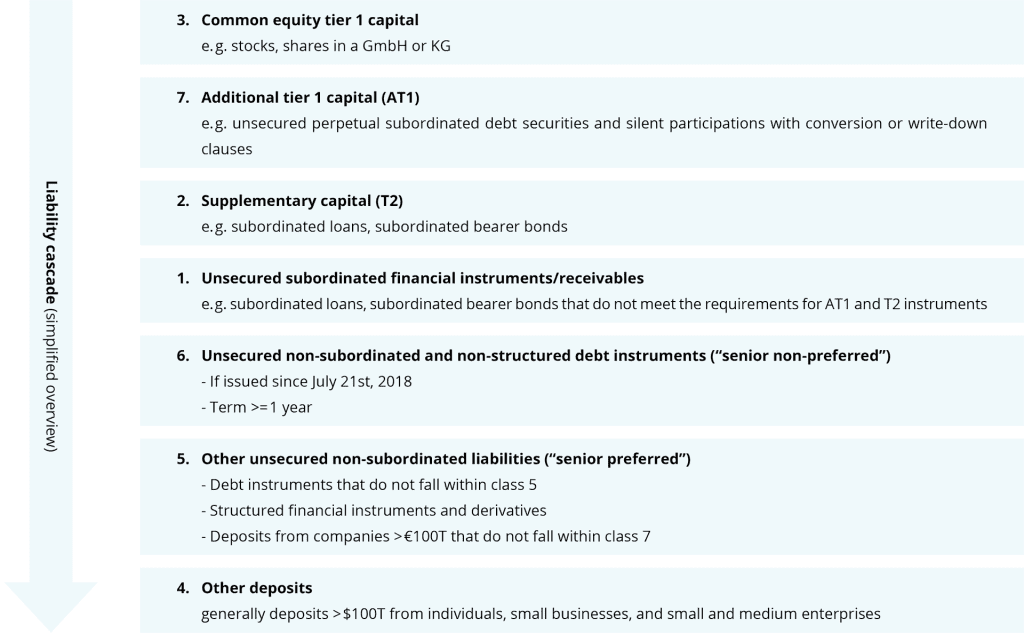

The question of whether creditors are affected by a bail-in resolution measure depends on the scope of the measure ordered and how their financial instrument or claim is classified. In the context of a bail-in, financial instruments and claims are divided into different classes and are subject to liability according to a statutory ranking (known as a “liability cascade”).

In terms of how shareholders and creditors of given classes are affected, the following principles apply: Only when a class of liabilities has been completely used and is not sufficient to compensate for losses to stabilize the bank, can the next class of liabilities in the liability cascade be accessed for write-downs or conversion into equity.

Certain types of financial instruments and receivables are legally exempt from the bail-in tool. These are, for example, deposits up to EUR 100,000 covered by the statutory deposit guarantee scheme and asset-backed liabilities (e.g. covered bonds). Liabilities to which a bail-in is applied are also referred to as eligible liabilities.

The liability cascade for German-based banks as of January 1st, 2017 is as follows:

- First, resolution measures are applied to common equity tier 1 capital and thus to the bank’s shareholders (i.e. owners of shares and other equity interests in the company).

- Next, the creditors of additional tier 1 capital (holders of unsecured perpetual subordinated debt securities and silent participations with conversion or write-down clauses that are subordinated to additional capital instruments) are affected.

- This is followed by utilization of tier 2 capital. This involves creditors of subordinated liabilities (e.g. holders of subordinated loans).

- Next in the liability cascade are unsecured subordinated financial instruments/receivables that do not meet the requirements for additional tier 1 capital or additional tier 2 capital.

- Next are unsecured non-subordinated financial instruments and receivables (“Other unsecured financial instruments/receivables”). This includes non-structured financial instruments/receivables such as: (a) Non-structured bonds and notes issued by public-sector entities, and rights comparable to these debt instruments that are tradable on the capital market in their own right, as well as registered bonds and promissory note loans, unless they fall into class (6) as deposits or are excluded from bail-in. This also includes financial instruments and receivables for which the amount of interest payments depends exclusively on a fixed or variable reference interest rate. (b) Liabilities in the form of structured, unsecured, non-subordinated financial instruments and receivables (“structured financial instruments/receivables”). Structured financial instruments/receivables are only included within this liability level after non-structured financial instruments/receivables. In the case of structured financial instruments and receivables (e.g. certificates on equity indices or receivables from derivatives), the amount of the repayment or interest payment depends on an uncertain future event or settlement is made by means other than cash. This also includes deposits of over EUR 100,000 from companies that do not fall into class (6).

- Finally, deposits made by private individuals, micro, small, and medium-sized enterprises may also be called upon if they exceed the statutory deposit guarantee of, in principle, EUR 100,000 (“Other Deposits”).

Effective from January 1st, 2017, the following simplified order of liability applies (direction of arrow), whereby a lower class is only called upon to bear losses if the preceding classes (starting with the common equity tier 1 capital) are not sufficient to bear losses:

How can the resolution measures affect me as a creditor?

If the resolution authority orders or takes a measure under these rules, the creditor may not terminate the financial instruments and claims or assert other contractual rights solely on the basis of this measure. This applies as long as the bank fulfills its main performance obligations under the terms of the financial instruments and receivables, including payment and performance obligations.

If the resolution authority takes measures as described, a total loss of the capital invested by shareholders and creditors is possible. Shareholders and creditors of financial instruments and receivables may therefore fully lose the purchase price paid for the acquisition of the financial instruments and receivables, as well as any other costs incurred in connection with the purchase.

The mere possibility that settlement measures may be ordered can make it more difficult to sell a financial instrument or a claim on the secondary market. This may mean that the shareholder and creditor can only sell the financial instrument or claim at a significant discount. Even if the issuing bank has existing repurchase obligations, the sale of such financial instruments may be at a substantial discount.

In a bank resolution, shareholders and creditors should not be left in a worse position than they would be in normal bank insolvency proceedings.

If the resolution measure nevertheless results in a shareholder or creditor being worse off than they would have been in normal insolvency proceedings against the bank, the shareholder or creditor may have a claim for compensation against the fund set up for resolution purposes (restructuring fund or single resolution fund, SRF). Should a compensation claim against the SRF arise, it is possible that payments resulting from this claim will be made significantly later than would have been the case had the bank properly fulfilled its contractual obligations.

Where can I find more information?

The German Federal Financial Supervisory Authority (BaFin), the FMSA, and the Deutsche Bundesbank have provided information on the restructuring and resolution rules applicable in Germany. You can also find more details here: https://www.bafin.de/SharedDocs/Veroeffentlichungen/DE/Merkblatt/BA/mb_haftungskaskade_bankenabwicklung.html

The FMSA has published a joint interpretative guidance with BaFin and Deutsche Bundesbank that provides further guidance on how money market instruments are to be determined and which debt instruments fall into class (5)(a) or (5)(b) as structured or non-structured financial instruments/claims: https://www.bafin.de/SharedDocs/Downloads/DE/Merkblatt/A/dl_Merkblatt_46f_KWG_nach_Konsultation_f_0205.pdf?__blob=publicationFile&v=3

iOS App Store

iOS App Store Google Play Store

Google Play Store